First, getting a loan can feel very stressful. However, you can make the process much easier. Specifically, you must understand your financial health. Therefore, learning how to read a credit report is absolutely essential. Indeed, your credit report decides if a bank will give you a loan. Additionally, it affects the exact interest rate you will pay. Consequently, a good report saves you a lot of money. Furthermore, many people ignore this highly important document.

As a result, they face loan rejections constantly. Luckily, you can change this negative outcome today. In this article, we will explain everything very clearly. For example, we will compare Experian and CIBIL. Similarly, we will show you how to read your credit report step by step. Thus, you will feel completely ready for your next loan application. Ultimately, this knowledge gives you immense financial power. Next, let us dive into the details right away.

What is a Credit Report?

Basically, a credit report is your financial report card. Specifically, it shows how you manage your borrowed money. For instance, it lists all your past personal loans. Moreover, it includes your current active credit cards. Furthermore, the report tracks your entire payment history. Because of this, lenders can easily see if you pay on time. Meanwhile, independent credit bureaus create these detailed reports. In India, four main bureaus do this important work. Namely, these are CIBIL, Experian, Equifax, and CRIF High Mark.

Naturally, each bureau gives you a three-digit numerical score. Usually, this score ranges directly from 300 to 900. Therefore, a higher score means much better financial health. Consequently, banks absolutely love high scores. Conversely, a low score makes banks worry a lot. As a result, they might reject your loan application immediately. Ultimately, you must check your credit report regularly. In fact, you can usually get one free report every single year. Therefore, you have zero excuse to ignore it.

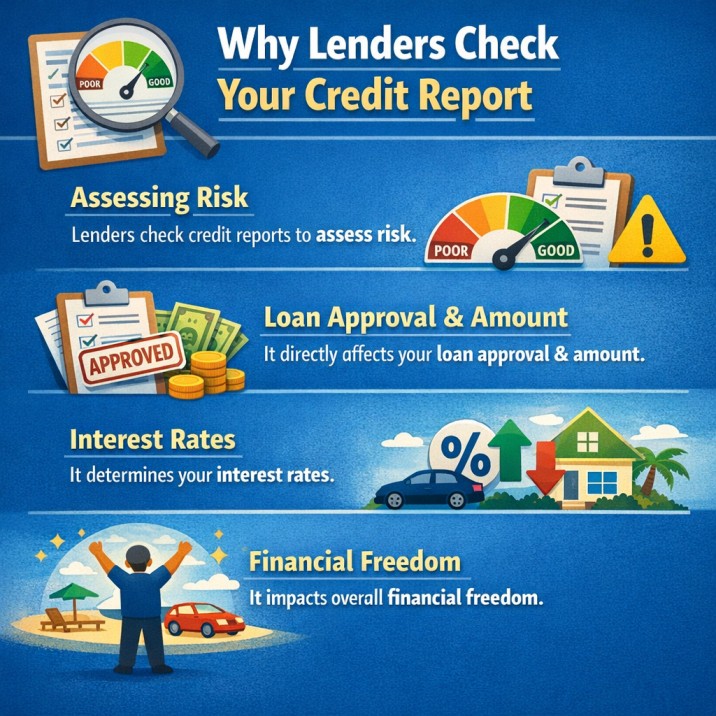

Why Lenders Check Your Credit Report

Primarily, lenders want to keep their own money completely safe. Therefore, they check your credit report very carefully. Because they desperately need proof of your financial reliability. After all, they do not know you personally at all. Consequently, the report acts as your financial character certificate. Furthermore, banks use it to decide your final loan amount. For example, a good report brings a massive loan limit. Alternatively, a bad report restricts your borrowing power heavily.

Additionally, lenders use the report to set your interest rates. Usually, high scores unlock much lower interest rates. As a result, you pay less extra money over time. Conversely, low scores directly lead to high interest rates. Thus, your monthly EMI payments become much higher. Moreover, credit card companies also look at this exact data. Similarly, they want to limit their financial risks. Ultimately, your credit report controls your financial freedom completely. Hence, keeping it healthy is extremely important for you. Without a doubt, it is the absolute key to easy loan approval.

CIBIL vs Experian: Key Differences

Now, let us compare the two biggest credit bureaus in India. Specifically, we will deeply look at CIBIL and Experian. Generally, both bureaus provide a highly detailed credit report. However, they have some very important differences. First, CIBIL is definitely the oldest bureau in India. Because of this, most traditional banks prefer CIBIL scores. On the other hand, Experian is newer but very fast.

Additionally, Experian updates fresh data more quickly. Furthermore, their secret scoring formulas differ slightly. Therefore, your score might be 750 on CIBIL but 780 on Experian. Even so, both scores are highly valid everywhere. Thus, you should check both reports if at all possible. Below, we have created a very simple comparison table. Consequently, you can see the main differences easily.

| Feature | CIBIL | Experian |

| Full Name | TransUnion CIBIL | Experian India |

| Score Range | 300 to 900 | 300 to 900 |

| Bank Preference | Very High | High |

| Data Update Speed | Standard | Very Fast |

| Good Score Level | Above 750 | Above 700 |

| Report Cost | One free per year | One free per year |

Ultimately, neither report is inherently better than the other. Instead, they just offer slightly different professional perspectives. Therefore, maintaining excellent habits benefits both scores equally.

Also Read: Cryptocurrency Tax In India 2026: 30% tax, TDS, VDA Rules Explained

How to Read Your Credit Report

Reading a credit report might seem confusing at first. However, it is actually a very simple task. Therefore, we will break it down into easy steps. First, look at your personal information section directly. Specifically, check your exact name, address, and PAN card number. Because tiny mistakes here can cause huge problems later. Second, find the specific account information section quickly. Here, the report clearly lists all your loans and credit cards. Moreover, it shows your total outstanding financial balances. Third, check your personal payment history very carefully.

Importantly, this is the single most critical part of your report. Mainly, it shows if you missed any monthly EMIs. Furthermore, look out for major red flags. For instance, words like “Written off” or “Settled” are extremely bad. Consequently, these negative remarks will ruin your loan chances entirely. Next, review the recent credit inquiries section. Basically, this shows who else checked your report recently. Too many hard inquiries will drop your score fast. Finally, check your overall three-digit score at the very top. Thus, you now successfully know how to read your report.

Spotting Errors on Your Credit Report

Sometimes, bureaus make accidental mistakes on your credit report. Unfortunately, these simple errors can hurt your score badly. Therefore, you must spot them very early. First, look for loans you never actually took. Because this could mean serious identity theft. Consequently, you must report this dangerous fraud immediately. Next, check for highly incorrect personal details. For example, a wrong address might mix your file with someone else’s file.

Furthermore, look very closely at your recorded payment history. Sometimes, you pay on time, but the report shows a delay. Because of this, your score drops completely unfairly. Therefore, you must gather your payment receipts right away. Afterwards, you can raise a formal dispute with the responsible bureau. Specifically, visit the official CIBIL or Experian website directly. Then, fill out their very simple online dispute form. Usually, they resolve these basic issues within thirty days. Ultimately, fixing these exact errors boosts your score quickly. Thus, your loan approval chances go up significantly.

How to Improve Your Credit Report

Building a incredibly strong credit report takes some real time. However, you can definitely do it with enough patience. First, always pay your EMIs exactly on time. Because payment history matters the absolute most to banks. Second, keep your overall credit utilization very low. Specifically, do not ever use your entire credit card limit. Instead, try to use only thirty percent of it. Therefore, banks will view you as a highly responsible borrower. Furthermore, do not apply for too many loans at once. Because each new application causes a hard inquiry.

Consequently, your score will drop slightly each single time. Additionally, maintain a very good mix of credit types. For example, have one secured loan and one unsecured credit card. Thus, lenders clearly see that you can handle different debts successfully. Moreover, keep your oldest credit cards fully active. Even if you rarely use them, keep them open. Because a long positive credit history looks very good. Ultimately, these incredibly simple habits will transform your report entirely. As a result, future loan approvals will become completely effortless.

Conclusion

In conclusion, deeply understanding your credit report is vital for your financial success. Initially, the many numbers and sections might seem very overwhelming. However, breaking them down makes everything much clearer. First, you learned exactly why strict banks care about your score.

Furthermore, we compared CIBIL and Experian for you easily. Therefore, you know exactly what modern lenders look for today. Additionally, we showed you how to spot hidden errors quickly. Consequently, you can fix them before applying for a new loan. Ultimately, your personal financial future is completely in your own hands. Thus, start checking your detailed report right away today. Always build exceptionally good habits, pay on time, and borrow wisely. As a result, you will never ever struggle with loan approvals again.

FAQs

How often should I check my credit report?

Generally, you should definitely check your credit report at least once a year. However, if you plan to take a big loan, check it six months in advance. Therefore, you have enough time to fix any dangerous errors.

Does checking my own score lower it?

No, checking your own personal score is just a soft inquiry. Consequently, it does not harm your score at all. Therefore, you can check it as often as you like safely.

Can a poor credit report be fixed?

Yes, absolutely. Furthermore, you can rebuild it easily by paying your bills exactly on time. Next, keep your outstanding balances very low constantly. Eventually, your score will steadily rise again over time.

Why is my Experian score higher than my CIBIL score?

Mainly, the two bureaus use slightly different math formulas. Additionally, they might update your data at totally different times. Therefore, minor score differences are completely normal and completely safe.

Also Read: Defense & Aerospace Mutual Funds: How Conflicts Drive 2026 Returns