Introduction

Are you confused about the difference between DSA and a Loan Agent? You’re not alone. Many people use these terms interchangeably. However, they represent different career paths in the financial services industry.

Understanding the difference between a Direct Selling Agent and a Loan Agent helps you make educated career decisions. Both roles concern selling financial products. Yet, they vary in their working technique, earnings, and responsibilities.

This complete guide describes everything you need to know. Let’s dive in and explore these exciting career opportunities.

Who is a DSA (Direct Selling Agent)?

A DSA (Direct Selling Agent) works as an authorized mediator for financial institutions. DSAs partner with banks, NBFCs, and fintech companies. They advertise and sell different loan products to the customers.

Who is a Loan Agent?

A loan agent generally works directly for a loan agency or a specific financial institution. They may receive a fixed salary plus incentives. Loan agents focus on selling products from their employer.

How DSAs Operate?

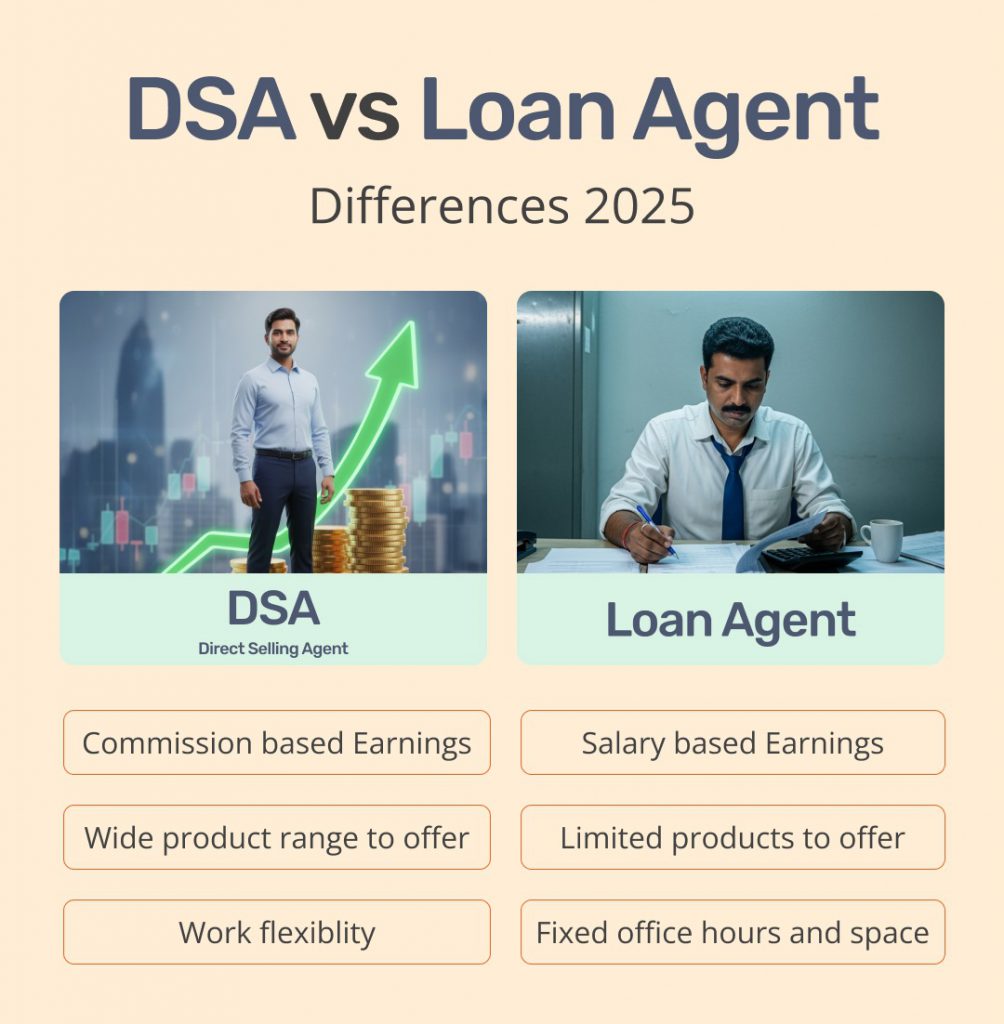

DSAs work alone under an agreement with financial institutions. They don’t receive a fixed salary. Instead, they earn commissions on successful loan disbursements.

The DSA model offers flexibility and freedom. You can work from anywhere and set your own schedule. Most DSAs build their own customer network over time.

Key characteristics of DSAs include:

- Earnings based on commission only

- Joining multiple financial institutions

- Manage the entire loan application process

- Maintain long-term customer relationships

- Focus on customer acquisition and retention

How Loan Agents Work?

Loan agents represent a single organization or a small group of lenders. They work within defined territories or branches. Their main goal is to achieve sales targets set by their employer.

Unlike DSAs, loan agents often have:

- Fixed monthly salary with performance bonuses

- Fixed product portfolio from one lender

- Restricted working hours and locations

- Supervision from the financial institutions

- Fixed sales targets

The loan agent role suits people who prefer stability and get a regular income regardless of monthly sales performance.

Key Differences Between DSA and Loan Agent

To understand the DSA and Loan Agent difference, let’s look at several key points. Here are the main differences.

Employment Status and Relationship

DSAs work as independent contractors. They’re not employees of any financial institution. Direct selling agents maintain a connection through formal agreements.

Loan agents typically have an employer-employee relationship. They work directly for loan agencies or banks. This provides job security and employment benefits.

Scope of Work and Product Range

A DSA can connect with multiple lenders simultaneously. This allows them to offer different loan products. Customers benefit from more options and competitive rates.

Loan agents represent one specific financial institution. They sell only their employer’s products. This limits customer preferences but ensures deep product knowledge.

Commission Structure and Earning Potential

DSAs earn purely based on commission. Their income depends completely on loan disbursements. High performers can earn quite a bit more than in salaried positions.

Loan agents receive fixed salaries plus variable incentives. This gives financial stability. However, their maximum earning potential may be limited.

Registration and Licensing Essentials

Both DSAs and loan agents need basic documentation. However, DSAs must register as business entities in many cases. They need PAN cards, GST registration, and partnership agreements.

Loan agents work under their employer’s license. The organization handles most regulatory submissions. Individual agents need fewer personal registrations.

Target Audience and Market Reach

DSAs can target any customer segment. They have the liberty to explore different markets. DSAs often specialize in specific slots over time.

Loan agents follow their organization’s target market strategy. They work within allotted regions. Their customer reach relies on company policies.

Independence and Flexibility

DSAs enjoy ultimate freedom. They decide their working hours, locations, and strategies. This flexibility attracts entrepreneurial people.

Loan agents work within organizational structures. They have to follow company guidelines and reporting systems. This has a clear direction but less autonomy.

Comparison Table: DSA vs Loan Agent

| Parameter | DSA (Direct Selling Agent) | Loan Agent |

| Employment Type | Independent | Employee |

| Income Structure | 100% commission-based | Fixed salary + incentives |

| Product Range | Multiple lenders & products | Single lender’s products |

| Working Hours | Flexible, self-determined | Fixed office hours |

| Work Location | Anywhere (home, field, office) | Office/assigned region |

| Investment Required | Minimal to none | None |

| Risk Level | Higher (No guaranteed salary) | Lower (guaranteed salary) |

| Earning Potential | Unlimited based on performance | Limited by salary structure |

| Registration | Business entity registration needed | Works under employer’s license |

| Independence | High liberation | Limited liberation |

| Training & Support | Self-learning + RM support | Comprehensive employer training |

| Job Security | Low (contract-based) | Higher (employment contract) |

| Growth Opportunity | Build own business network | Climb corporate ladder |

| Target Market | Self-chosen customer segments | Company-defined segments |

| Relationship with Lender | Partnership agreement | Employment relationship |

Roles and Responsibilities

| Responsibility | DSA (Direct Selling Agent) | Loan Agent |

| Customer Acquisition | Actively search for potential customer through networking, referrals, & marketing. Build own customer base independently. | Identify prospects within assigned region. Follow company’s lead generation guidelines. |

| Product Consultation | Inform customers about multiple loan options from different lenders. Compare products to find the best fit for the customers. | Promote the organization’s loan products only. Explain features, benefits, and terms of the employer’s products solely. . |

| Application Processing | Help customers complete loan applications independently. Ensure all documents are accurate and complete before submission. | Process applications through internal company systems. Ensure compliance with company policies and procedures. |

| Verification Support | Work with customers during verification processes. Encourage communication between borrowers and multiple lenders. | Coordinate verification through company channels. Handle verification as per organizational protocols. |

| Documentation Assistance | Guide customers in collecting required documents from various lenders. Provide support for multiple loan applications. | Help customers collect documents as per company requirements. Verify information before internal submission. |

| Target Achievement | Set own performance goals and targets. Income depends entirely on self-determined performance levels. | Meet monthly sales targets set by management. Work towards specific KPIs assigned by employer. |

| Relationship Management | Build long-term relationships with customers independently. Maintain contact for future business and referrals. | Maintain customer relationships as per company standards. Handle queries and complaints through organizational channels. |

| Market Research | Identify and explore new market opportunities. Choose target customer segments based on personal strategy. | Work within company-defined market segments. Follow organizational marketing and outreach strategies. |

Eligibility and Requirements

How to Become a DSA?

Starting as a direct selling agent requires:

Age Criteria: You must be at least 18 years old.

Education: Most lenders require a minimum high school education. Some prefer graduates.

Documents: You need a PAN card, Aadhaar card, and address proof. Business registration may be necessary.

Bank Account Details: An active bank account is essential for receiving commissions.

Communication Skills: Strong interpersonal skills help you succeed. You should explain financial products clearly.

Investment: Minimal to no initial investment is needed. However, marketing expenses may arise.

Registration Process: Connect with financial institutions through their DSA programs. Complete their onboarding requirements.

How to Become a Loan Agent?

Joining loan agencies requires:

Educational: Most organizations prefer graduates. Some accept experienced candidates with lower qualifications.

Age Criteria: Candidates should be between 21-35 years typically. Age limits vary by organization.

Experience: Prior sales experience helps but isn’t always mandatory. Freshers can apply for entry-level positions.

Documents: Basic identity and address proofs are sufficient. Educational certificates are required.

Interview Process: Pass the organization’s selection process. This includes aptitude tests and interviews.

Training: Complete the mandatory training program. Learn about products, processes, and compliance.

Advantages and Disadvantages

Pros and Cons of Being a DSA

Advantages:

- Unlimited Earning Potential: Income grows with performance. Top DSAs earn particularly more than salaried positions.

- Flexibility: Work according to one’s own schedule. Freedom to choose work location and methods.

- Multiple Income Sources: Connect with several lenders simultaneously. Diversified product portfolio.

- Business Ownership: Can build own brand and network. Create long-term business value.

- No Income Cap: Hard work instantly translates to higher income.

Disadvantages:

- Income Uncertainty: Monthly earnings vary based on performance. Some months may yield low income.

- No Fixed Benefits: DSAs don’t receive medical insurance or paid leave.

- Self-Motivation Required: Success depends completely on effort. No manager is pushing you daily.

- Initial Struggle: Building a customer base takes time. Early months may be financially challenging.

- Competition: Many DSAs compete for the same customers. Standing out requires unique strategies.

Pros and Cons of Being a Loan Agent

Advantages:

- Fixed Monthly Income: Receive a guaranteed salary irrespective of performance.

- Employee Benefits: Get medical insurance, paid leave, and other perks. Organizations provide extensive benefits.

- Training: Receive professional training from the employer.

- Career Progression: Can move into managerial roles over time.

- Job Security: Employment contracts provide stability. Performance-based terminations are less common.

Disadvantages:

- Limited Earning Potential: Your maximum income is limited by the salary structure. Outstanding performance may not much increase earnings.

- Fixed Working Hours: Must work according to office timings. Restricted flexibility.

- Limited Product Range: Sell only the employer’s products. Can’t offer customers multiple options.

- Less Independence: Follow organizational policies strictly.

- Region Restrictions: Work within assigned areas only. Expanding beyond limits isn’t permitted.

Which One Should You Choose?

Choosing between DSA and loan agent depends on your personality and goals. Consider these factors carefully.

Choose DSA If You:

- Focus on unlimited earning potential

- Choose flexible working hours

- Appreciate entrepreneurial challenges

- Hold strong self-motivation

- Can manage income instabilities

- Desire to build your own business

- Own good networking skills

- Desire long-term wealth creation

Choose a Loan Agent If You:

- Choose financial stability

- Enjoy a fixed monthly income

- Require employee benefits

- Choose structured work environments

- Desire corporate career growth

- Desire professional training

- Require job security

- Choose working in teams

Benefits of Partnering with or joining WeRize

- Easy Onboarding

- Competitive Commissions

- Multiple Products

- Technology Support

- Training & Resources

- Quick Payouts

- Dedicated Support

How to Register with WeRize

- Download the WeRize Partner App from the Google Play Store

- Sign in using your mobile number

- Complete OTP verification

- Select “Sell WeRize loans to other customers”

- Fill in your personal details and PAN information

- Complete Aadhaar verification if required

- Capture your selfie for identity verification

- Add your bank account details

- Start selling and earning immediately

You get a platform for your success. Join thousands of DSAs already earning with us.

Conclusion

The DSA and loan agent difference comes down to independence v/s stability. DSA enjoys flexibility and unlimited earnings. While Loan agents benefit from fixed income and job security.

Understanding loan agencies and their operations helps you make informed decisions. Both career paths offer special advantages. Choice should align with personality, goals, and financial situation.

The direct selling agent instance suits entrepreneurial individuals. If you prefer building your own business, DSA is your path. If you value corporate structure and steady income, consider becoming a loan agent.

Remember, success in either role requires dedication and hard work. The financial services industry rewards those who serve customers well. Choose the path that excites you most.

Ready to start your journey? WeRize offers opportunities. Join our platform today and begin your career in financial services. Your success story starts here.

Frequently Asked Questions

Q1: Is a DSA the same as a loan agent?

No, they’re different. DSAs work separately as partners with numerous lenders. Loan agents are employees of specific loan agencies. The DSA and loan agent differences include employment status, income structure, and work flexibility.

Q2: Can I work as both a DSA and a loan agent simultaneously?

Generally, no. Most loan agencies restrict employees from working as DSAs for other financial institutions. This creates a conflict of interest. However, transition is always there from one role to another over time.

Q3: Which pays better – DSA or loan agent?

It depends on the performance. Top-performing DSAs earn much more than loan agents. However, DSA income fluctuates monthly. Loan agents have a guaranteed fixed income. High performers succeed as DSAs, while those preferring stability choose loan agent positions.

Q4: Do I need a license to become a DSA or loan agent?

DSAs need partnership agreements with lenders. Some require business registration. Loan agents work under their employer’s license. Individual licenses aren’t required for loan agents. Conditions vary by organization and state regulations.

Q5: What is the main difference between a direct selling agent and a loan agent?

The main difference is independence. DSA works as an individual with various lenders. Loan agents are employees of single organizations. DSAs have flexible working conditions while loan agents follow company policies.

Q6: How do loan agencies differ from DSA partnerships?

Loan agencies are financial institutions that employ loan agents directly. They provide fixed salaries and benefits. DSA partnerships involve contractual agreements between independent agents and lenders. DSAs don’t receive employee benefits or fixed salaries.

Q7: Can I switch from a loan agent to a DSA later?

Yes, many people transition to DSA after gaining experience as loan agents. This transition is common. You gain valuable knowledge about loan products and processes as a loan agent. This experience helps you succeed as a DSA.

Q8: Which role has better career growth opportunities?

Both offer different growth paths. Loan agents can progress to senior positions within loan agencies. They may become team leaders or branch managers. DSAs build their own business networks. They can establish loan agencies someday. Decide based on whether you prefer corporate growth or entrepreneurial development.

Q9: Do DSAs and loan agents need different skills?

Core skills are similar for both. You need good communication, sales ability, and customer service skills. However, DSAs need stronger self-motivation and business management skills. Loan agents need better teamwork and policy adherence abilities. Understanding the DSA and loan agent differences helps you develop the right skills.