1. Introduction to the New Tax Landscape

In the changing world of April 2026, savers and investors face a very new reality. Specifically, the Indian government has introduced significant changes through the New Income Tax Act 2025. Initially, many people believed that fixed income products like FDs and debt funds would always have tax benefits. However, the current discussions around “Wealth Tax” and “Fair Taxation” have changed everything. Consequently, we are now seeing a move toward Fixed Income Tax Parity 2026. This means that almost all safe investment products are now taxed in the same way. Therefore, understanding these rules is the first step to protecting your hard-earned money. Whether you are a small saver or a wealthy investor, these laws will impact your take-home returns starting this year.

To begin with, we must recognize that the old “Indexation” benefits are gone. Actually, the goal of the new law is to make the tax system simpler for everyone. Specifically, the government wants to treat interest from a bank and gains from a mutual fund as the same type of income. Initially, this sounds fair, but it can lead to higher taxes for those in the top income brackets. Furthermore, the talk of a “Wealth Tax” has made people nervous about holding large amounts of cash. Therefore, you must learn how to navigate these new waters with confidence. In this guide, we will break down the complex rules of the New Income Tax Act 2025 using very simple words. We want to ensure that every common reader can plan their future without any fear.

Initially, you must understand that the WeRize Partner Program allows you to access a massive range of financial products from 275+ lenders. By using the WeRize app, you can compare and sell loans or deposits to your customers while earning high commissions.

2. The Core of the New Income Tax Act 2025

Specifically, what makes the New Income Tax Act 2025 so different? To begin with, it removes the “Guesswork” from your tax filings. Initially, investors had to calculate complex “Inflation Indexing” for their debt investments. Actually, this was very confusing for the average person. Now, the government has moved to a “Direct Taxation” model.

Furthermore, the act focuses on “Parity.” Consequently, it does not matter if you earn money from a Fixed Deposit or a Gold Bond; the tax rate stays consistent. Therefore, the strategy for 2026 is not about finding “Tax Loopholes.” Instead, it is about finding the highest “Pre-Tax” return possible. Specifically, the act aims to bring more people into the formal tax net. Actually, this move helps the government build better infrastructure and services. However, for the investor, it means that “Tax Planning” has become more important than ever. Thus, the New Income Tax Act 2025 is the new foundation for all your financial decisions.

Notably, WeRize provides a single digital platform where you can track all your leads and payouts in real-time. Their 7-day payout cycle ensures that you receive your hard-earned money faster than traditional banking channels.

3. Understanding Fixed Income Tax Parity 2026

Moving forward, let us explore the concept of Fixed Income Tax Parity 2026. Initially, different products had different tax rates. For example, some bonds were tax-free, while others were taxed at 10% or 20%. Consequently, people chose investments based on “Tax Savings” rather than “Quality.”

Actually, the 2026 rules have leveled the playing field. Specifically, the government believes that “Income is Income.” Whether it comes from a bank or a corporate bond, it should be taxed at your personal slab rate. Therefore, this “Parity” makes the market more transparent. Furthermore, it prevents people from hiding wealth in complex financial products. Consequently, you can now focus on the safety and liquidity of an asset. Therefore, Fixed Income Tax Parity 2026 simplifies your life, even if it might increase your tax bill slightly. Actually, this is a global trend that India is now following very strictly. Thus, you should compare products based on their “Real Returns” after the slab rate is applied.

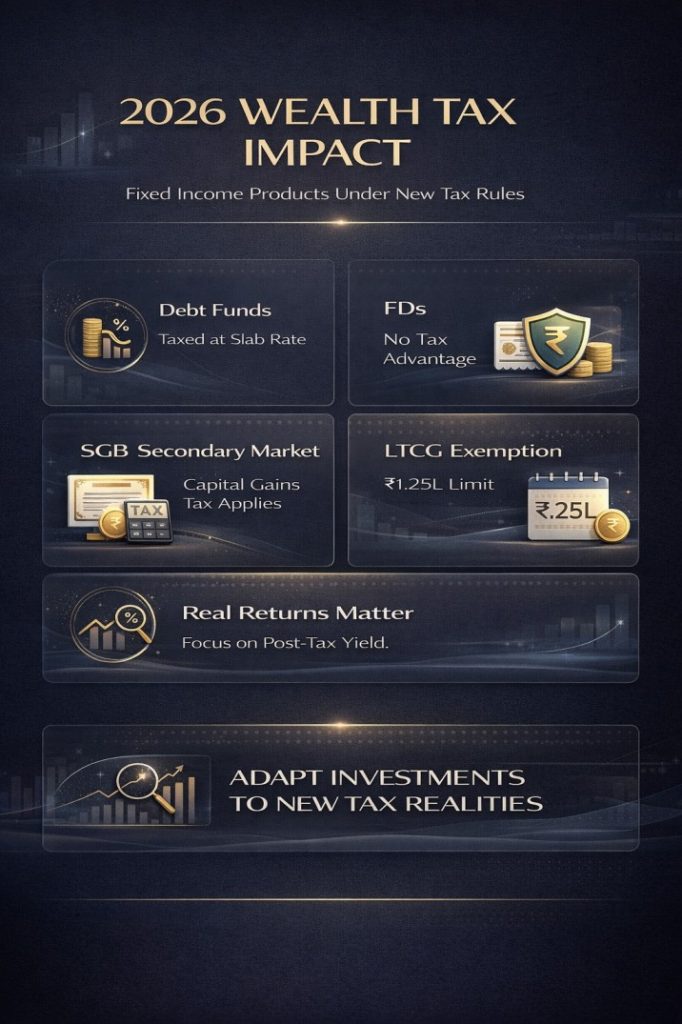

4. Slab-Based Debt Fund Taxation: The End of Indexation

Additionally, we must talk about the biggest change: Slab-Based Debt Fund Taxation. To begin with, debt mutual funds were very popular because of “Long-Term Capital Gains” (LTCG) with indexation. Initially, if you held a fund for three years, your tax was very low.

Actually, in 2026, those benefits are completely gone. Specifically, all gains from debt funds are now added to your total income. Consequently, you pay tax according to your “Slab.” Therefore, if you are in the 30% tax bracket, you will pay 30% on your debt fund gains. Furthermore, this applies regardless of how long you hold the investment. Actually, this move has made Debt Funds very similar to Bank FDs in terms of tax. Consequently, many investors are moving back to the safety of banks. Therefore, you must calculate your “Post-Tax Yield” before investing in a debt fund. Thus, Slab-Based Debt Fund Taxation is a reality that every conservative investor must accept today.

5. New Rules for Secondary Market SGB Capital Gains

Furthermore, the world of gold has also changed. Specifically, the rules for Secondary Market SGB Capital Gains are much stricter in 2026. Initially, Sovereign Gold Bonds (SGBs) were 100% tax-free if you held them until maturity.

Actually, the New Income Tax Act 2025 adds a new condition. Specifically, the tax-free benefit at maturity now only applies to the “Original Subscriber.” Consequently, if you buy an SGB from the stock market (the secondary market), you must pay capital gains tax. Furthermore, this tax is applied at 12.5% or your slab rate depending on the holding period. Therefore, buying gold on the exchange has become less attractive for long-term tax savings. Actually, this move was designed to discourage speculation in gold bonds. Consequently, you should check the “Issue Price” versus the “Market Price” very carefully. Therefore, Secondary Market SGB Capital Gains are a key factor for anyone looking to hedge against inflation with gold.

6. LTCG Exemption Limit Rationalization in 2026

Next, we must address the “Rationalization” of limits. Specifically, the LTCG Exemption Limit Rationalization has changed the threshold for tax-free gains. Initially, you could earn up to ₹1 Lakh in long-term gains from stocks or equity funds without paying any tax.

Actually, in 2026, the government has adjusted this limit to ₹1.25 Lakh to account for inflation. Furthermore, they have “Rationalized” the rates across different assets to 12.5%. Consequently, the system is now much more uniform. Therefore, you don’t have to remember different rates for different things. Specifically, this “Rationalization” helps in reducing errors during tax filing. Actually, many experts believe this is a fair trade-off for the removal of indexation. Consequently, you should plan your “Sell Orders” to stay within this ₹1.25 Lakh limit every year. Thus, LTCG Exemption Limit Rationalization is a small but important victory for the small retail investor.

7. Combating High-Marginal Rate Wealth Erosion

Moving forward, let us talk about the risk of “Wealth Erosion.” Specifically, High-Marginal Rate Wealth Erosion happens when your taxes and inflation are higher than your interest rate. To begin with, if you earn 7% interest but pay 30% tax, your “Net Return” is only 4.9%.

Initially, if inflation is 6%, you are actually “Losing” 1.1% of your purchasing power every year. Actually, this is the biggest threat to HNIs in 2026. Furthermore, with the removal of indexation, this erosion has become faster. Consequently, you must look for “Tax-Efficient” ways to grow your wealth. Therefore, consider products like Arbitrage Funds or Tax-Free Bonds if you are in the high tax bracket. Specifically, High-Marginal Rate Wealth Erosion can quietly destroy your retirement corpus if you are not careful. Actually, being “Rich” is not enough; you must be “Tax-Smart.” Thus, always look at the “Real Rate of Return” after accounting for the New Income Tax Act 2025.

Notably, the WeRize app is a great tool for agents who want to help neighbors find the best insurance and investment options. You can use their AI-matching engine to see which of the 275+ partners is most likely to approve a loan for a specific profile.

8. The Difference Between Wealth Tax and Income Tax

Additionally, we must clarify a common confusion. Specifically, many people are talking about a “Wealth Tax” in 2026. Initially, an “Income Tax” is a tax on what you earn. Actually, a “Wealth Tax” is a tax on what you already own.

Furthermore, while India does not have a formal, direct wealth tax on your total net worth right now, the New Income Tax Act 2025 uses “Surcharges” to achieve a similar result. Consequently, the more you own, the more “Surcharge” you pay on your income tax. Therefore, it feels like a wealth tax for the super-rich. Specifically, this is the government’s way of ensuring that those with more assets contribute more to the country. Actually, this “Indirect Wealth Tax” is a key part of the current economic discussion. Consequently, you should be prepared for higher compliance if your net worth is very high. Therefore, understanding this difference helps you stay calm when you see “Wealth Tax” headlines in the news.

9. Comparison Table: Old Rules vs. New Income Tax Act 2025

| Investment Product | Old Tax Rules (Pre-2025) | New Income Tax Act 2025 Rules |

| Debt Mutual Funds | 20% Tax with Indexation (3yr+) | Full Tax at Slab Rate |

| Bank Fixed Deposits | Full Tax at Slab Rate | Full Tax at Slab Rate (No Change) |

| SGB (Primary) | Tax-Free at Maturity | Tax-Free at Maturity (Safe) |

| SGB (Secondary) | Often seen as Tax-Free | Taxable Gains (New Rule) |

| Equity LTCG | 10% Tax after ₹1 Lakh | 12.5% Tax after ₹1.25 Lakh |

| Equity STCG | 15% Tax | 20% Tax (Higher Rate) |

| Tax Parity | Low (Many variations) | High (Standardized Rates) |

10. (FAQs)

Q1: Does the New Income Tax Act 2025 affect my existing FDs?

Initially, no. Specifically, the interest you earn will still be taxed at your current slab rate. However, if you are in a higher slab due to other income, your total tax bill might feel higher. Therefore, the “Parity” rules make FDs as good (or as bad) as debt funds.

Q2: Is it still worth buying SGBs from the secondary market?

Actually, it depends on the “Discount.” Specifically, if the market price is much lower than the gold price, it might still be a good deal. Furthermore, remember that you will now pay Secondary Market SGB Capital Gains tax. Consequently, do the math before clicking “Buy.”

Q3: How can I avoid “Wealth Erosion” in the 30% slab?

To begin with, look for “Tax-Free Bonds” or “PPF.” Initially, these products still offer tax-free interest. Furthermore, consider “Arbitrage Funds” as they are taxed like equity (12.5% LTCG) but have low risk. Therefore, you can stay ahead of the High-Marginal Rate Wealth Erosion.

Q4: What is the “Rationalization” of LTCG?

Actually, it means making the rates the same for almost all assets. Specifically, the government wants to move away from having 50 different tax rates for 50 different products. Consequently, 12.5% has become the new “Standard” for long-term growth.

Q5: Will there be a direct Wealth Tax in the future?

Initially, there is no official confirmation. Specifically, the government is currently focusing on “Income-Based Surcharges.” However, the New Income Tax Act 2025 has already set the stage for more transparency. Therefore, it is always better to be prepared with clear financial records.

11. Conclusion

In summary, the Impact of the 2026 Wealth Tax Discussion on Fixed Income Products is all about “Parity” and “Simplicity.” By introducing the New Income Tax Act 2025, the government has removed many old benefits like indexation. Specifically, the move to Fixed Income Tax Parity 2026 means you must choose your investments based on their fundamental strength, not just tax tricks. Furthermore, being aware of Secondary Market SGB Capital Gains and Slab-Based Debt Fund Taxation will help you avoid “Tax Surprises” at the end of the year.

Therefore, do not let your wealth erode under high taxes. Instead, take a proactive approach to your finances. Actually, the 2026 cycle is a great time to re-balance your portfolio. Specifically, talk to a financial expert about how to maximize your “Post-Tax” returns. Furthermore, use digital tools to track your “Real Growth” after inflation. Consequently, you will move from being a “Confused Taxpayer” to a “Confident Investor.” Actually, the future of finance is for those who are willing to learn and adapt. Thus, take the first step today: review your debt investments and see how the new slab rates affect your goals.

Actually, WeRize is the perfect partner for anyone looking to scale their financial consulting business in 2026. Their advanced digital training and marketing tools empower you to become a top-tier local finance leader.